How to pay Yourself as a sole proprietor

How to Pay Yourself as a Sole Proprietor

Paying yourself as a sole proprietor seems simple, but how you pay yourself can affect your taxes and cash flow more than you might think. When you DIY your bookkeeping, it’s easy to mix personal and business money or miss hidden tax rules.

Understanding the right way to pay yourself helps you protect your business, stay on the IRS’s good side, and know exactly where your money goes. You’ll learn how to keep things straight with your bookkeeping and avoid tax headaches later on.

With a simple routine and smart habits, you can pay yourself the right way and gain more control over your business money.

Table of Contents

Understanding Sole Proprietorship Income

Running a business as a sole proprietor means your personal and business finances are deeply connected, even if they feel like separate worlds. Every dollar that comes in counts as your own, but knowing how money flows from your business to your pocket makes a big difference for taxes and bookkeeping. Get clear on what you need to track, and paying yourself becomes a lot less stressful.

What Counts as Business Income?

When you collect payments from customers, that money starts out as gross income. Gross income is the total amount your business earns before you pay for anything like supplies, rent, or advertising. It’s the big number at the top of your sales report.

But you don’t get to keep all of that. After you pay your bills, buy materials, and cover other “cost of doing business” expenses, what’s left is your net income (sometimes called profit). This is the money you actually have available to pay yourself and set aside for taxes.

Here’s a quick snapshot:

Gross income: All money your business brings in.

Business expenses: Money you spend to keep the business running (supplies, marketing, rent).

Net income: What’s left after expenses, your real take-home pay as the owner.

Only net income is money you can safely pay yourself, not gross. Mixing up these two numbers can leave you short when it’s time to pay bills or taxes. Treat your business profit like the pool you draw from—not every dollar that comes in.

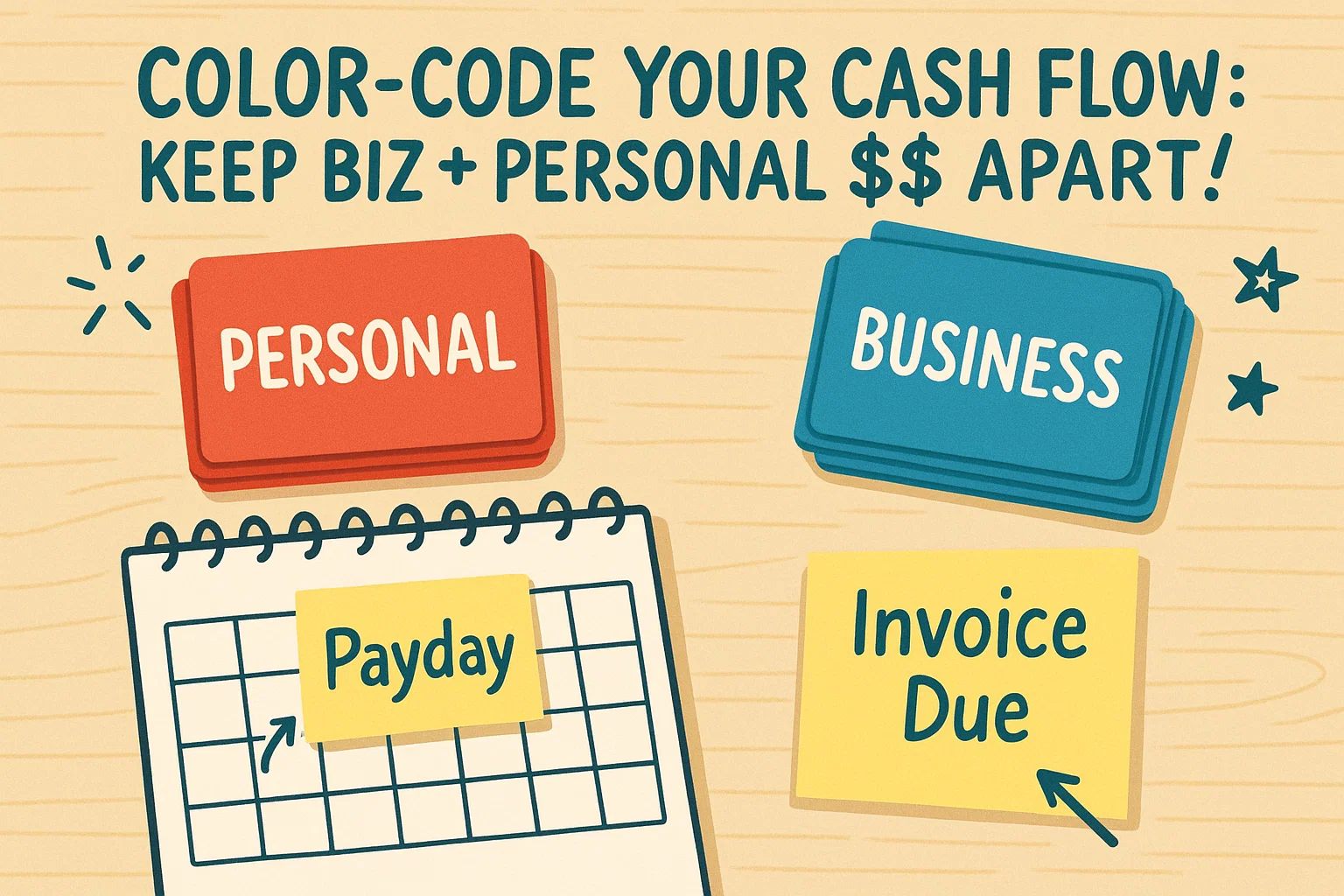

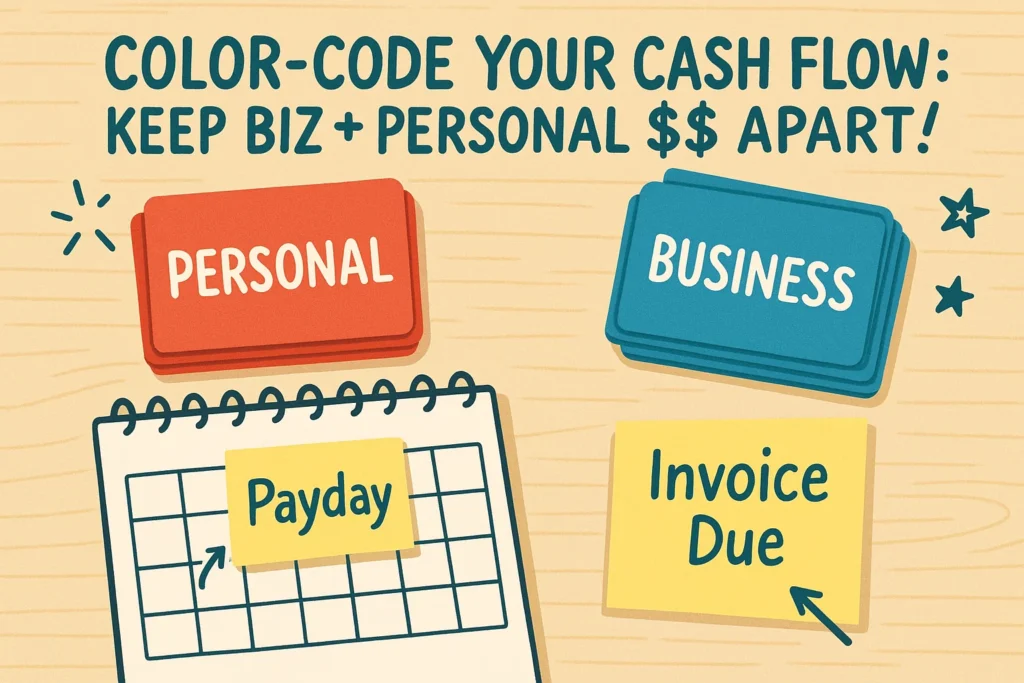

Personal vs. Business Accounts

Even though the IRS sees you and your business as the same person, using separate bank accounts is not only a smart move, it’s essential. Keeping business and personal money apart can make your bookkeeping simple and save you headaches at tax time.

Why have distinct accounts? Here’s what you gain:

- Clean, easy records: It’s simpler to track what the business earned and spent.

- Fewer mix-ups: Personal purchases don’t sneak into business expenses, avoiding confusion later.

- Better tax preparation: Clear separation makes tax time smoother, with less digging for receipts.

- Professionalism: Businesses that keep finances separate look more reliable to clients and lenders.

Having separate bank accounts brings real peace of mind. It’s kind of like putting up a fence between your yard and your business; you’ll always know which side the money belongs on.

When it’s time to pay yourself, just move money from your business account to your personal one.

Record the transfer as an “owner’s draw.” This habit protects your bookkeeping and keeps your business running smoothly.

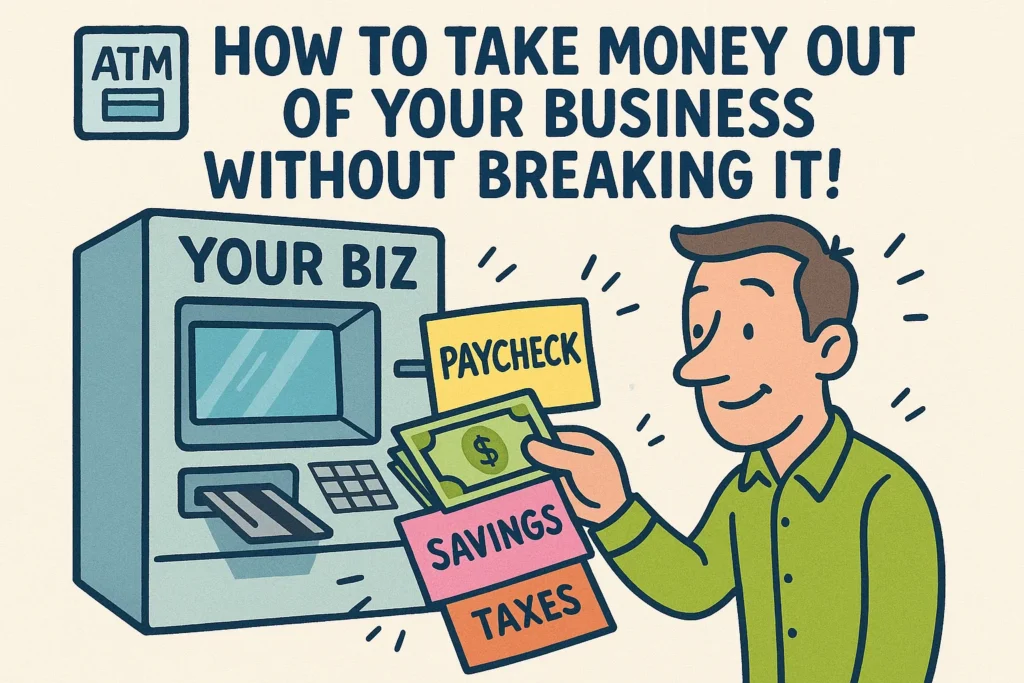

How to Legally Pay Yourself as a Sole Proprietor

As a sole proprietor, paying yourself is straightforward, but following a clear method keeps your business healthy and your tax records clean. The owner’s draw is the best-known approach. It’s simple, flexible, and matches how the IRS sees your business income.

Here’s how the process works and how to handle moving money from your business account to your personal one without creating confusion.

What Is an Owner’s Draw?

An owner’s draw is how you take money out of your business for personal use when you’re a sole proprietor. Instead of getting a set paycheck, you move profits to your personal account as you need them.

There’s no payroll system or withholdings for Social Security or Medicare like you’d have if you were an employee.

How does an owner’s draw work in real life?

Picture this: Your business account has a profit for the month after covering all expenses. You want to pay yourself. You pull out some or all of that money—this act is called an “owner’s draw.”

A few things to know about owner’s draws:

You decide how much to take and when, based on what the business can afford.

There’s no tax withheld up front. Instead, you pay self-employment taxes and income tax later, most often through quarterly estimated payments.

Every draw should be tracked in your bookkeeping. Record it as “owner’s draw” or “owner distribution” to show it’s not a business expense.

Think of it like dipping into your business’s piggy bank. You’re just moving your own money from one jar to another, but you need to keep a clean record each time you do.

What you DO NOT DO is pay for personal things from your business bank account and count that as paying yourself. Absolutely not. STOP right there. Do NOT pass go.

How to Transfer Funds

Moving money from your business account to your personal account is simple, but it pays to build a habit out of doing it the right way. The cleaner your transfers, the easier tax time will be.

Before making a transfer, check your net income. Only withdraw what your business can afford, leaving enough to cover bills, taxes, and future expenses.

Here’s a step-by-step process you can follow:

- Decide on the amount. Base your draw on your net profit, not your total sales. Take what you need, but leave enough for business obligations.

- Pick a schedule. You can pay yourself as needed, but regularity brings predictability. Many owners transfer weekly, biweekly, or monthly. Find what fits your cash flow.

- Choose your method. You have options:

- Bank transfer: Move funds electronically from your business to your personal account. Fast, easy to document, and traceable.

- Paper check: Write yourself a check from your business account and deposit it into your personal one. Good for those who like paper trails.

- Cash withdrawal: Not recommended unless there’s no other option. Cash is hard to track and can muddy your records.

- Record the draw. Always log the transfer in your books as an “owner’s draw” or similar label. Keep it out of your expense list; it doesn’t reduce your taxable business income. How to Set Up a Simple Bookkeeping System — Even If You Hate Numbers

- Store the proof. Save bank statements, check images, or transfer confirmations so you can back up every draw if the IRS comes calling.

A few best practices make this process smoother:

- Make transfers from business to personal accounts only, never directly pay personal bills from the business account.

- Don’t exceed your available profit. Overdrawing can leave your business short and complicate your records.

- Stick to digital methods or checks for a clear paper trail.

By sticking to these habits, you simplify your own bookkeeping, keep audit worries low, and build trust in your numbers—both for you and for your accountant.

Don’t forget to check out The 7 Most Common Bookkeeping Mistakes (and How to Avoid Them) and if you need to find a bookkeeping software to get started, we compared them for you! Comparing Bookkeeping Software.

A quick reminder than an excellent resource is the IRS’s small business and self-employed tax center for the rules straight from the official source. https://www.irs.gov/businesses/small-businesses-self-employed